At Benchmark, we continually monitor the market and your loan, so you don’t have to. This way, you are offered the perfect product for your position, and we strive to always get you the best mortgage possible.

At Benchmark, we continually monitor the market and your loan, so you don’t have to. This way, you are offered the perfect product for your position, and we strive to always get you the best mortgage possible.FIND YOUR BRANCH

Learning Center

Buying a home can seem like a daunting task, but it doesn’t have to be one. This is the Benchmark University. Browse, learn, and enjoy the journey to your new home.

Our Core Values

Our core values drive our culture, shape our paradigm, and have been the foundation of our success. It’s one thing to promise great service; at Benchmark, we bake it right in.

![]()

We Give Back

We make an impact beyond the mortgage industry. We honor wounded veterans, promote their support, and help them re-integrate into successful civilian life.

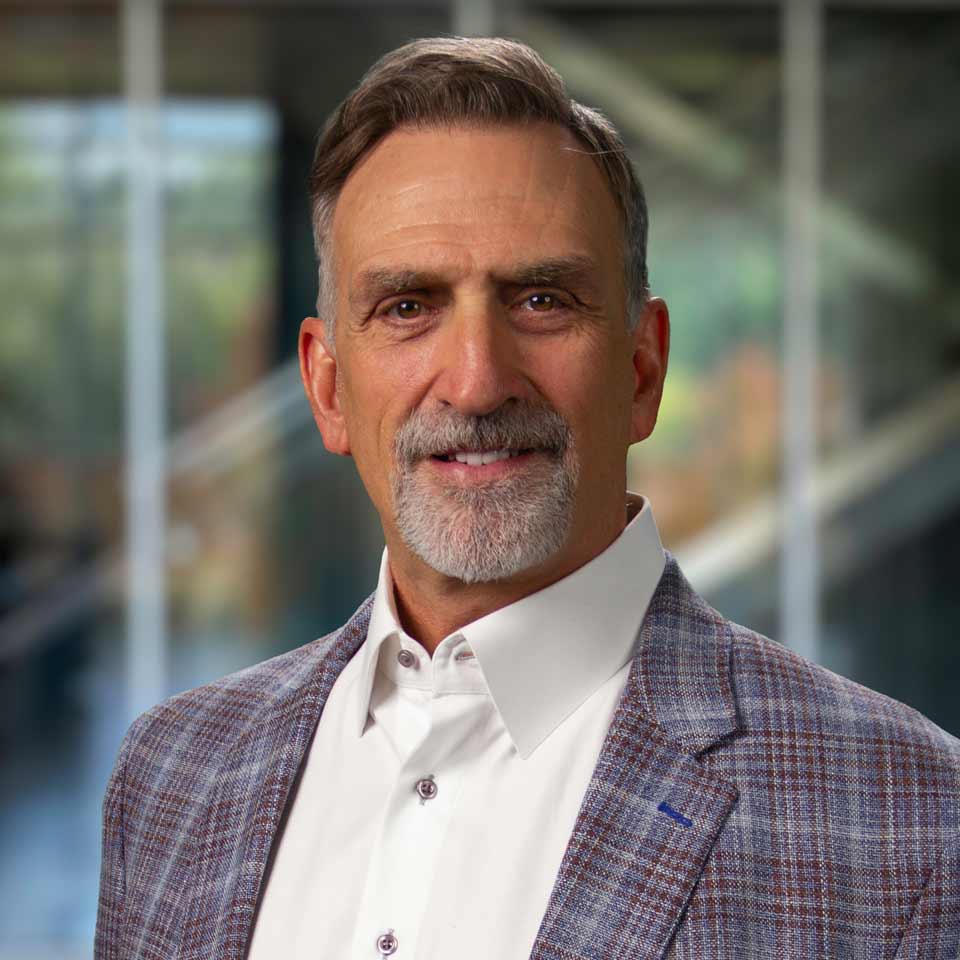

Jim McMahan Welcomes You to Benchmark

Welcome to Benchmark,

Benchmark is a remarkable community of mortgage professionals. At Benchmark, we have a clearly defined set of core values that we live out and practice every day. Having carefully selected each team member one person at a time, and with an average of over a decade of individual experience, we have assembled what we believe is the best team in the mortgage industry today. Not only does our team go the extra mile to serve our branches, loan officers, and support teams, we also stand ready to deliver an exceptional experience that is second to none for our customers. Please reach out and let us know if we can help you take advantage of the Benchmark opportunity today.

Jim McMahan | President